Back to News

Is Private Credit Showing Cracks? What the Numbers Say

Private credit’s move into the financial mainstream has brought heightened scrutiny. But while headlines suggest broad-based pressure, the data tells a more differentiated story, with risk concentrated in specific segments and outcomes increasingly driven by manager discipline as deal competition rises.

For much of the past decade, private credit has been one of the big winners of institutional portfolios. Its combination of stable income and limited exposure to public market volatility has pushed the asset class from niche to mainstream. Today, private corporate credit represents a roughly $2 trillion US market, rivaling the size of the publicly traded high yield and syndicated loan markets, and now plays an increasingly important role in how companies raise capital.

But recently, that rapid growth has drawn scrutiny. A series of high-profile defaults and greater use of payment-in-kind (PIK) interest have raised questions about the health of credit markets and whether private credit is facing deeper, systemic issues.

We see those concerns as overblown, driven more by headlines than by careful analysis. While some segments of private credit are encountering challenges, the broader data points to an asset class working through growing pains rather than exhibiting signs of systemic distress. Much of the current anxiety is framed by a one-size-fits-all view of private credit, ignoring how uneven risk is and how widely results can vary across strategies.

How the Narrative Took Shape

Concern about private credit has intensified as several structural and cyclical forces have converged at the same time. The most visible has been the pace of asset growth. Private credit has tripled in size in the past five years, pulling in capital from institutions, family offices, and high-net-worth investors seeking yield and diversification. Periods of aggressive growth inevitably invite questions around underwriting discipline and capital quality, particularly when competition for deals intensifies and terms begin to loosen.

Those questions have only grown louder as the interest rate environment has shifted dramatically over the last several years. Borrowers that were comfortably servicing debt at near-zero rates suddenly faced interest expense that doubled or tripled. That transition naturally exposed weaker balance sheets, particularly among more leveraged companies with limited pricing power.

Against that backdrop, a small number of high-profile problem credits moved into the spotlight. The bankruptcy of used-car dealer Tricolor and the collapse of auto parts supplier First Brands were idiosyncratic events, yet were frequently cited as evidence of broader stress in private credit. In reality, both situations primarily involved publicly traded debt rather than private credit exposures. While headline-grabbing, these cases say far more about a narrow set of issuers than about a private credit market that has fundamentally changed in scope and structure over the past decade.

What the Headlines Get Right

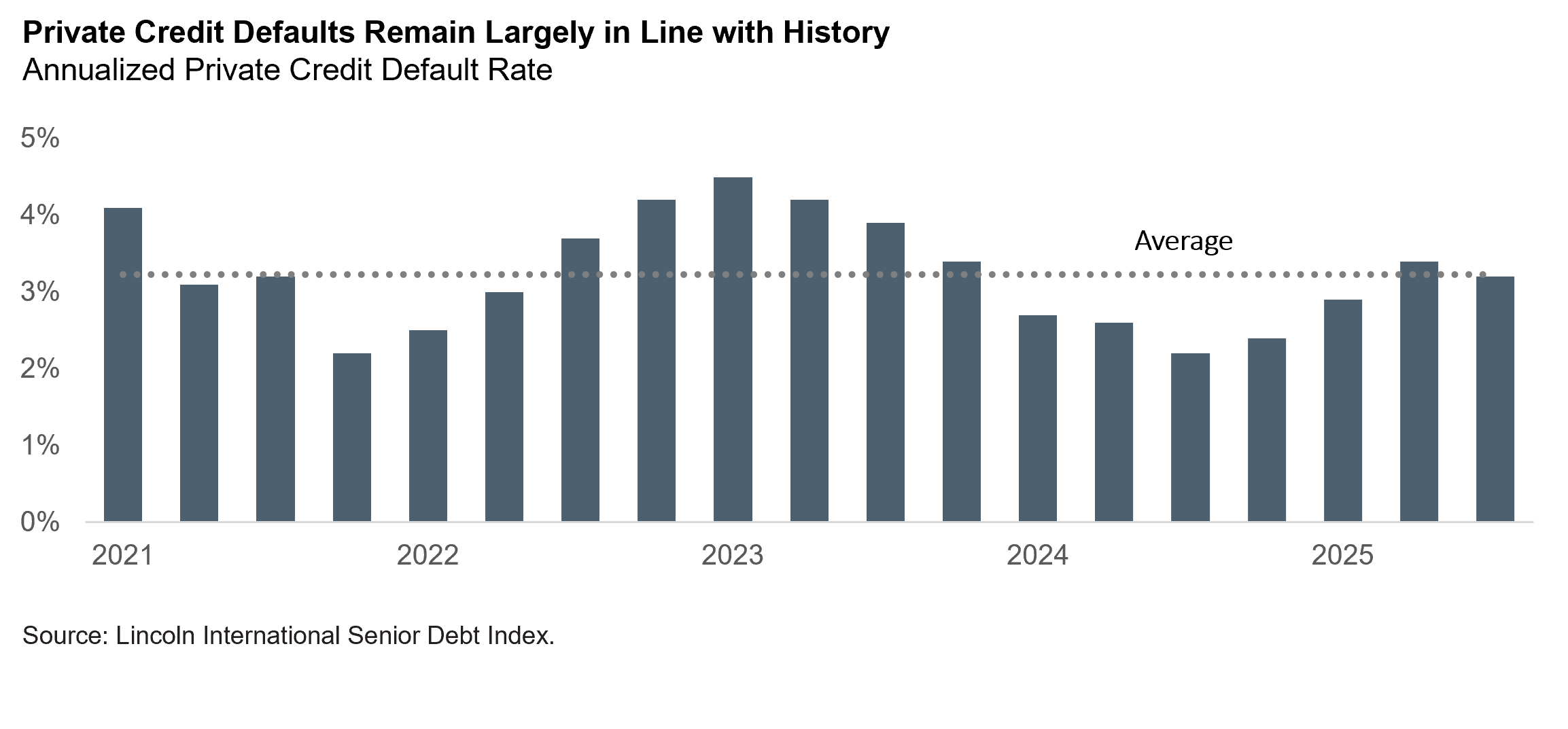

It’s no secret that defaults are on the rise as the market resets from its post-pandemic lows. In a market spanning thousands of loans, some level of credit stress is inevitable as rates normalize and weaker borrowers are tested. What matters is where they are occurring and how severe the losses really are. A closer look shows that much of the stress is concentrated in a narrow set of sectors, and in loans originated at the peak of the 2021–2022 market when competition was the most intense and terms were looser.

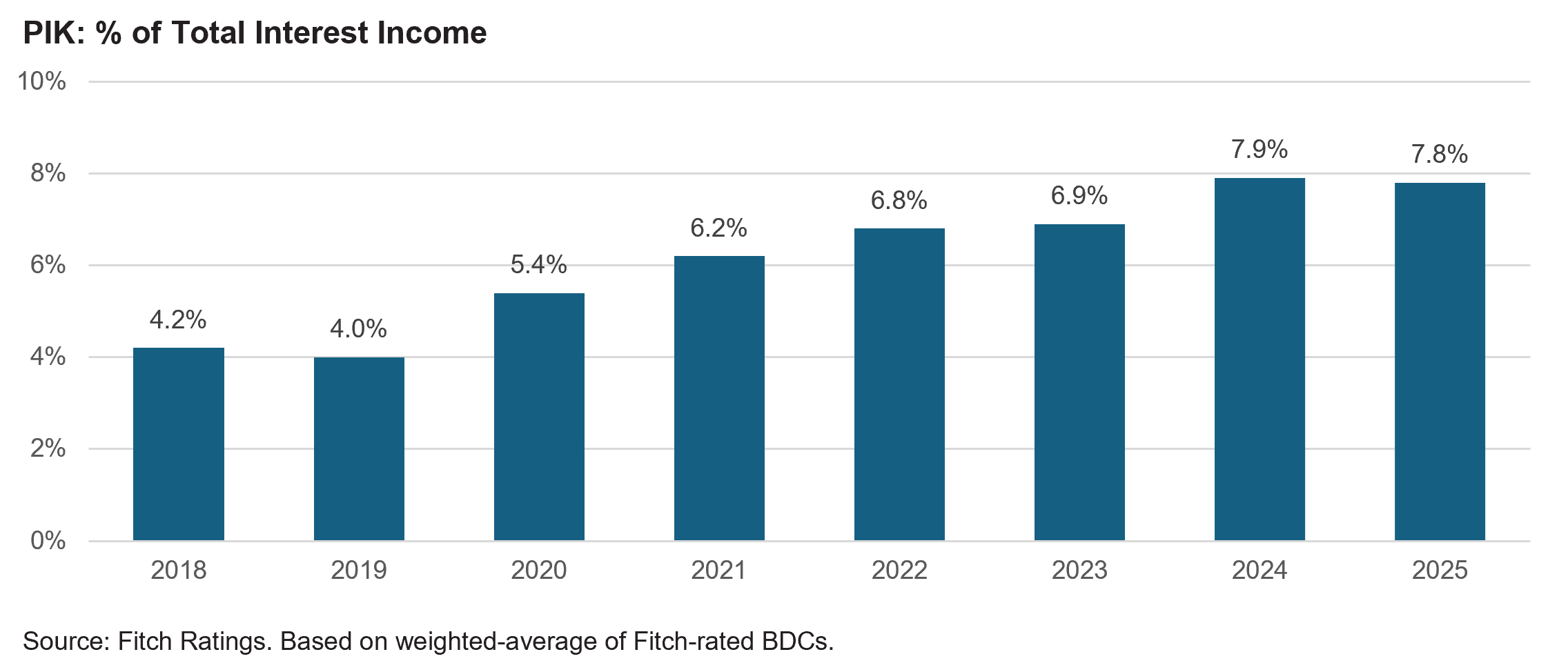

That same dynamic has fueled increased attention on PIK interest—a nuanced tool across credit markets that allows borrowers to defer interest payments by adding them to the loan’s principal balance. As interest rates increased and cash flows tightened since 2022, more borrowers chose to preserve liquidity by paying a portion of interest at maturity rather than entirely in cash. Critics argue this practice masks underlying credit stress, effectively treating PIK usage as a “shadow default” that keeps reported default rates artificially low.

Rising PIK usage can signal borrower stress, but on its own it is not evidence of weakening private credit fundamentals. PIK has long been used selectively to manage liquidity needs, strategically to free up working capital to help companies grow and scale. But a broad increase in PIK usage across portfolios may indicate mounting pressure on borrowers and merits closer scrutiny. The risk ultimately lies not in the use of PIKs themselves, but in a manager’s ability to distinguish between strategic PIK and stress-driven PIK—a distinction that is critical for performance and portfolio stability.

A Closer Look: What the Data Actually Shows

When examined alongside public credit markets, private credit fundamentals look far more resilient than the headlines suggest. Default rates have inevitably risen from cycle lows, but they remain broadly comparable to, and in some cases below, those in public high yield and leveraged loan markets. Even within direct lending, stress has been uneven, with materially different outcomes by borrower size and loan profile. Importantly, when stress does emerge, private credit’s senior-secured positioning and greater lender control provide borrowers with options to limit losses and preserve value.

Concerns around PIK interest have similarly attracted attention, yet the data suggests usage remains contained. Public filings from business development companies (BDCs), a reasonable proxy for private credit fundamentals, show that PIK exposure averages roughly 8% of portfolios. That figure has modestly risen since 2022 when interest rates began to normalize. More notably, when looking across the landscape, that figure is skewed by a small number of managers with more aggressive strategies or higher concentrations of 2021–2022 vintages, where equity cushions have eroded. In practice, PIK usage is highly sponsor- and strategy-dependent and should be looked as a strategic tool for bridging borrower underperformance, making proactive monitoring essential for preserving value.

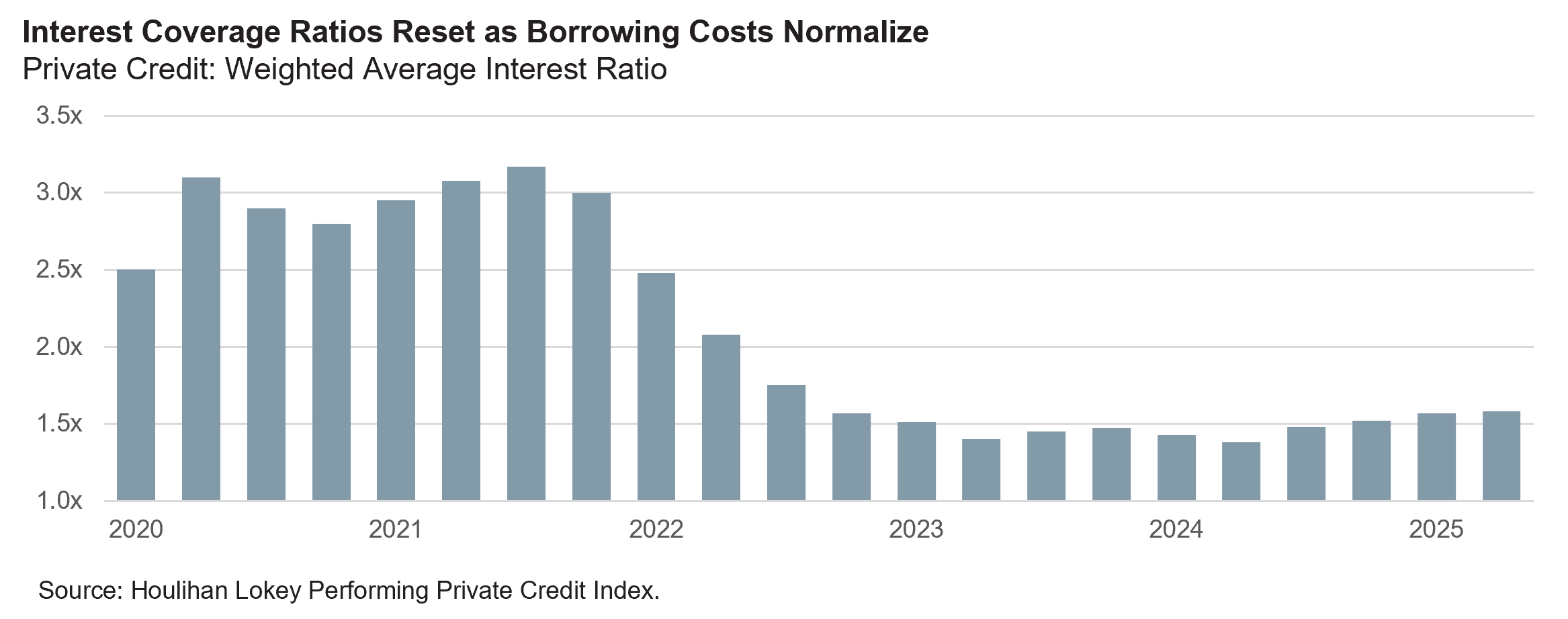

Interest coverage ratios have also declined but this, too, reflects a normal adjustment to a period of higher interest rates. Importantly, this trend has stabilized as companies adjusted cost structures and passed through pricing where possible. As interest rates normalize, further relief may follow. That said, lower rates alone will not resolve deeper structural challenges in stressed credits.

Not All Private Credit is Created Equal

Perhaps the most important distinction missing from the broader debate is that private credit is not a single, uniform asset class. In reality, private credit spans a range of assets, lending types, and structures, with performance and risk outcomes reflecting this. Established platforms with disciplined underwriting standards and long-standing sponsor relationships are navigating the current environment very differently than more aggressive entrants that scaled rapidly during the peak of the cycle in order to deploy capital.

That dispersion also reflects differences in access and execution. Managers with consistent deal flow have been able to remain selective, which means stronger terms and better downside structure. Experience managing stressed credits and workouts has also become increasingly valuable as conditions have tightened. In this context, dispersion is a defining feature of the asset class, reinforcing that manager and strategy selection will ultimately determine results.

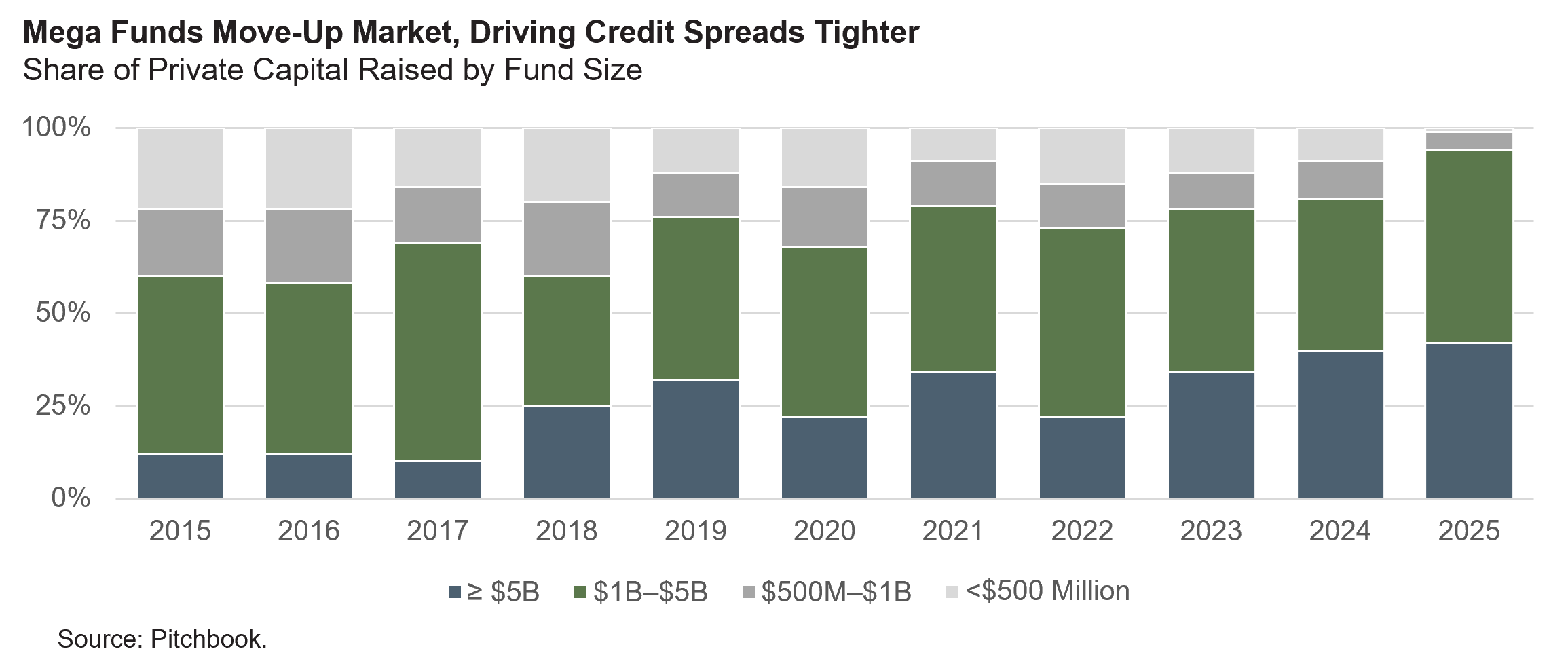

Competitive dynamics have further widened that gap. Across direct lending, large pools of dry powder are chasing a limited set of deals, pushing lenders to compete more aggressively on both pricing and structure, particularly in sponsor-backed deals. The impact has been most pronounced in the upper middle market, where transactions are larger and increasingly compete directly with the syndicated loan market. In these segments, spreads have compressed and lender protections have weakened.

By contrast, core middle market lending has remained somewhat more insulated, reflecting lower competition and more bespoke origination. The lower middle market, where Crescent Grove Advisors prefers to deploy capital, continues to offer a premium for complexity, even as increased competition has narrowed the historical gap. Importantly, this segment typically features lower leverage, stronger lender protections, and more attractive full-cycle risk-adjusted return potential. In this environment, maintaining valuation discipline and prioritizing structure are essential as competitive pressures continue to build.

What to Watch For

The economic backdrop remains full of crosscurrents. Tariffs, monetary policy shifts, and persistent inflation are working through the system. While headline credit stats look acceptable, a certain level of complacency has overcome investors. Equity market valuations are full and most things feel “priced to perfection”, and it’s rational for any investor to reassess where they’re taking risk. Today’s environment of geopolitical tensions and inflationary pressures, driven by everything from deficit spending to trade, can create pockets of volatility overnight.

Within credit markets, elevated deal activity is creating both opportunity and risk. Increased origination provides a larger opportunity set, but it is occurring alongside heightened competition and tighter spreads. In this environment, selectivity matters. Manager discipline around structure and lender protections is critical, especially as pressure to deploy capital increases.

At the same time, innovation is reshaping pockets of the opportunity set. Accelerating investment in artificial intelligence and related infrastructure is creating new financing demand, with mega-cap technology issuers accessing markets in ways that were uncommon in prior cycles. These developments warrant close scrutiny, with a focus on pricing and durability of cash flows.

Putting It All Together

The gap between private credit headlines and underlying fundamentals remains wide. Recent defaults and rising PIK usage reflect a market adjusting to the new normal of higher interest rates. The current environment is exposing weaker structures and more aggressive underwriting decisions made at the peak of the cycle.

Private credit is functioning as intended, but under less forgiving conditions. Going forward, outcomes will be determined less by broad asset class exposure and more by manager approach and selectivity. For investors, the distinction between temporary stress and permanent impairment is critical. Failing to separate the two can cause investors to overlook where the real risks and real opportunities lie.

Disclosures

This material is intended for general informational purposes only. This should not be considered an individualized recommendation or personalized investment advice.

Past performance is not a guarantee of future performance, and all investments are subject to the risk of loss.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from is obtained from what are considered reliable third-party sources. However, its accuracy, completeness or reliability cannot be guaranteed.

This information is not a specific recommendation, individualized tax, legal, or investment advice. Tax laws are subject to change, either prospectively or retroactively. Where specific advice is necessary or appropriate, individuals should contact their own attorney or tax to help answer questions about specific their specific situations or needs prior to taking any action based upon this information.

Download PDF

Is Private Credit Showing Cracks? What the Numbers Say

Feb 06, 2026 | Insights

Private credit’s move into the financial mainstream has brought heightened scrutiny. But while headlines suggest broad-based pressure, the data tells a more differentiated story, with risk concentrated in specific segments and outcomes increasingly driven by manager discipline as deal competition rises.

For much of the past decade, private credit has been one of the big winners of institutional portfolios. Its combination of stable income and limited exposure to public market volatility has pushed the asset class from niche to mainstream. Today, private corporate credit represents a roughly $2 trillion US market, rivaling the size of the publicly traded high yield and syndicated loan markets, and now plays an increasingly important role in how companies raise capital.

But recently, that rapid growth has drawn scrutiny. A series of high-profile defaults and greater use of payment-in-kind (PIK) interest have raised questions about the health of credit markets and whether private credit is facing deeper, systemic issues.

We see those concerns as overblown, driven more by headlines than by careful analysis. While some segments of private credit are encountering challenges, the broader data points to an asset class working through growing pains rather than exhibiting signs of systemic distress. Much of the current anxiety is framed by a one-size-fits-all view of private credit, ignoring how uneven risk is and how widely results can vary across strategies.

How the Narrative Took Shape

Concern about private credit has intensified as several structural and cyclical forces have converged at the same time. The most visible has been the pace of asset growth. Private credit has tripled in size in the past five years, pulling in capital from institutions, family offices, and high-net-worth investors seeking yield and diversification. Periods of aggressive growth inevitably invite questions around underwriting discipline and capital quality, particularly when competition for deals intensifies and terms begin to loosen.

Those questions have only grown louder as the interest rate environment has shifted dramatically over the last several years. Borrowers that were comfortably servicing debt at near-zero rates suddenly faced interest expense that doubled or tripled. That transition naturally exposed weaker balance sheets, particularly among more leveraged companies with limited pricing power.

Against that backdrop, a small number of high-profile problem credits moved into the spotlight. The bankruptcy of used-car dealer Tricolor and the collapse of auto parts supplier First Brands were idiosyncratic events, yet were frequently cited as evidence of broader stress in private credit. In reality, both situations primarily involved publicly traded debt rather than private credit exposures. While headline-grabbing, these cases say far more about a narrow set of issuers than about a private credit market that has fundamentally changed in scope and structure over the past decade.

What the Headlines Get Right

It’s no secret that defaults are on the rise as the market resets from its post-pandemic lows. In a market spanning thousands of loans, some level of credit stress is inevitable as rates normalize and weaker borrowers are tested. What matters is where they are occurring and how severe the losses really are. A closer look shows that much of the stress is concentrated in a narrow set of sectors, and in loans originated at the peak of the 2021–2022 market when competition was the most intense and terms were looser.

That same dynamic has fueled increased attention on PIK interest—a nuanced tool across credit markets that allows borrowers to defer interest payments by adding them to the loan’s principal balance. As interest rates increased and cash flows tightened since 2022, more borrowers chose to preserve liquidity by paying a portion of interest at maturity rather than entirely in cash. Critics argue this practice masks underlying credit stress, effectively treating PIK usage as a “shadow default” that keeps reported default rates artificially low.

Rising PIK usage can signal borrower stress, but on its own it is not evidence of weakening private credit fundamentals. PIK has long been used selectively to manage liquidity needs, strategically to free up working capital to help companies grow and scale. But a broad increase in PIK usage across portfolios may indicate mounting pressure on borrowers and merits closer scrutiny. The risk ultimately lies not in the use of PIKs themselves, but in a manager’s ability to distinguish between strategic PIK and stress-driven PIK—a distinction that is critical for performance and portfolio stability.

A Closer Look: What the Data Actually Shows

When examined alongside public credit markets, private credit fundamentals look far more resilient than the headlines suggest. Default rates have inevitably risen from cycle lows, but they remain broadly comparable to, and in some cases below, those in public high yield and leveraged loan markets. Even within direct lending, stress has been uneven, with materially different outcomes by borrower size and loan profile. Importantly, when stress does emerge, private credit’s senior-secured positioning and greater lender control provide borrowers with options to limit losses and preserve value.

Concerns around PIK interest have similarly attracted attention, yet the data suggests usage remains contained. Public filings from business development companies (BDCs), a reasonable proxy for private credit fundamentals, show that PIK exposure averages roughly 8% of portfolios. That figure has modestly risen since 2022 when interest rates began to normalize. More notably, when looking across the landscape, that figure is skewed by a small number of managers with more aggressive strategies or higher concentrations of 2021–2022 vintages, where equity cushions have eroded. In practice, PIK usage is highly sponsor- and strategy-dependent and should be looked as a strategic tool for bridging borrower underperformance, making proactive monitoring essential for preserving value.

Interest coverage ratios have also declined but this, too, reflects a normal adjustment to a period of higher interest rates. Importantly, this trend has stabilized as companies adjusted cost structures and passed through pricing where possible. As interest rates normalize, further relief may follow. That said, lower rates alone will not resolve deeper structural challenges in stressed credits.

Not All Private Credit is Created Equal

Perhaps the most important distinction missing from the broader debate is that private credit is not a single, uniform asset class. In reality, private credit spans a range of assets, lending types, and structures, with performance and risk outcomes reflecting this. Established platforms with disciplined underwriting standards and long-standing sponsor relationships are navigating the current environment very differently than more aggressive entrants that scaled rapidly during the peak of the cycle in order to deploy capital.

That dispersion also reflects differences in access and execution. Managers with consistent deal flow have been able to remain selective, which means stronger terms and better downside structure. Experience managing stressed credits and workouts has also become increasingly valuable as conditions have tightened. In this context, dispersion is a defining feature of the asset class, reinforcing that manager and strategy selection will ultimately determine results.

Competitive dynamics have further widened that gap. Across direct lending, large pools of dry powder are chasing a limited set of deals, pushing lenders to compete more aggressively on both pricing and structure, particularly in sponsor-backed deals. The impact has been most pronounced in the upper middle market, where transactions are larger and increasingly compete directly with the syndicated loan market. In these segments, spreads have compressed and lender protections have weakened.

By contrast, core middle market lending has remained somewhat more insulated, reflecting lower competition and more bespoke origination. The lower middle market, where Crescent Grove Advisors prefers to deploy capital, continues to offer a premium for complexity, even as increased competition has narrowed the historical gap. Importantly, this segment typically features lower leverage, stronger lender protections, and more attractive full-cycle risk-adjusted return potential. In this environment, maintaining valuation discipline and prioritizing structure are essential as competitive pressures continue to build.

What to Watch For

The economic backdrop remains full of crosscurrents. Tariffs, monetary policy shifts, and persistent inflation are working through the system. While headline credit stats look acceptable, a certain level of complacency has overcome investors. Equity market valuations are full and most things feel “priced to perfection”, and it’s rational for any investor to reassess where they’re taking risk. Today’s environment of geopolitical tensions and inflationary pressures, driven by everything from deficit spending to trade, can create pockets of volatility overnight.

Within credit markets, elevated deal activity is creating both opportunity and risk. Increased origination provides a larger opportunity set, but it is occurring alongside heightened competition and tighter spreads. In this environment, selectivity matters. Manager discipline around structure and lender protections is critical, especially as pressure to deploy capital increases.

At the same time, innovation is reshaping pockets of the opportunity set. Accelerating investment in artificial intelligence and related infrastructure is creating new financing demand, with mega-cap technology issuers accessing markets in ways that were uncommon in prior cycles. These developments warrant close scrutiny, with a focus on pricing and durability of cash flows.

Putting It All Together

The gap between private credit headlines and underlying fundamentals remains wide. Recent defaults and rising PIK usage reflect a market adjusting to the new normal of higher interest rates. The current environment is exposing weaker structures and more aggressive underwriting decisions made at the peak of the cycle.

Private credit is functioning as intended, but under less forgiving conditions. Going forward, outcomes will be determined less by broad asset class exposure and more by manager approach and selectivity. For investors, the distinction between temporary stress and permanent impairment is critical. Failing to separate the two can cause investors to overlook where the real risks and real opportunities lie.

Disclosures

This material is intended for general informational purposes only. This should not be considered an individualized recommendation or personalized investment advice.

Past performance is not a guarantee of future performance, and all investments are subject to the risk of loss.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from is obtained from what are considered reliable third-party sources. However, its accuracy, completeness or reliability cannot be guaranteed.

This information is not a specific recommendation, individualized tax, legal, or investment advice. Tax laws are subject to change, either prospectively or retroactively. Where specific advice is necessary or appropriate, individuals should contact their own attorney or tax to help answer questions about specific their specific situations or needs prior to taking any action based upon this information.

Download PDF